The Wealth Stack: The Six Layers Nobody Mapped Together

A walk through the six layers underneath every family office — data, infrastructure, operating system, behaviour, business model, future — and how to tell which one is actually broken when something goes wrong.

Meera, a partner at a multi-family office in Bangalore, asked her team one question about the Mehta family at 9am on a Tuesday. “What’s their total equity exposure?” A routine question, for an 11am call.

She had three answers by lunch. ₹47cr, ₹52cr, ₹61cr.

She had seen the firm’s numbers disagree before. The last time, the gap had cost the Mehtas something they could not buy back. She just didn’t connect the two until later.

The analyst who pulled the first number had used the consolidated portfolio tracker, which is fed by CAS but doesn’t include the two PMS allocations. The second number came from the wealth manager’s quarterly statement, which includes the PMS but values an unlisted block at the founder’s last private round — eighteen months stale. The third came from the in-house Excel that the family’s old auditor maintains. That sheet includes a 14% stake in an unlisted manufacturing entity the family has, in any practical sense, already written off, but technically still owns through an HUF that nobody has touched since 2019.

None of these people were wrong. They were each answering a slightly different question on a slightly different version of the truth, and the question wasn’t specific enough to surface the disagreement.

This happens every week.

Most of the conversation about wealth-tech treats this as a software problem. Bad UI. Slow reports. Fragmented dashboards. The fix sold is usually a better software or a better dashboard. But when the same question gets three different answers from your own team, the dashboard isn’t the problem. It’s just the last place the problem shows up.

Here is the whole essay in one line: the layer you can see is the cheapest one to fix, so it is the one you keep fixing — and it is almost never where the break is.

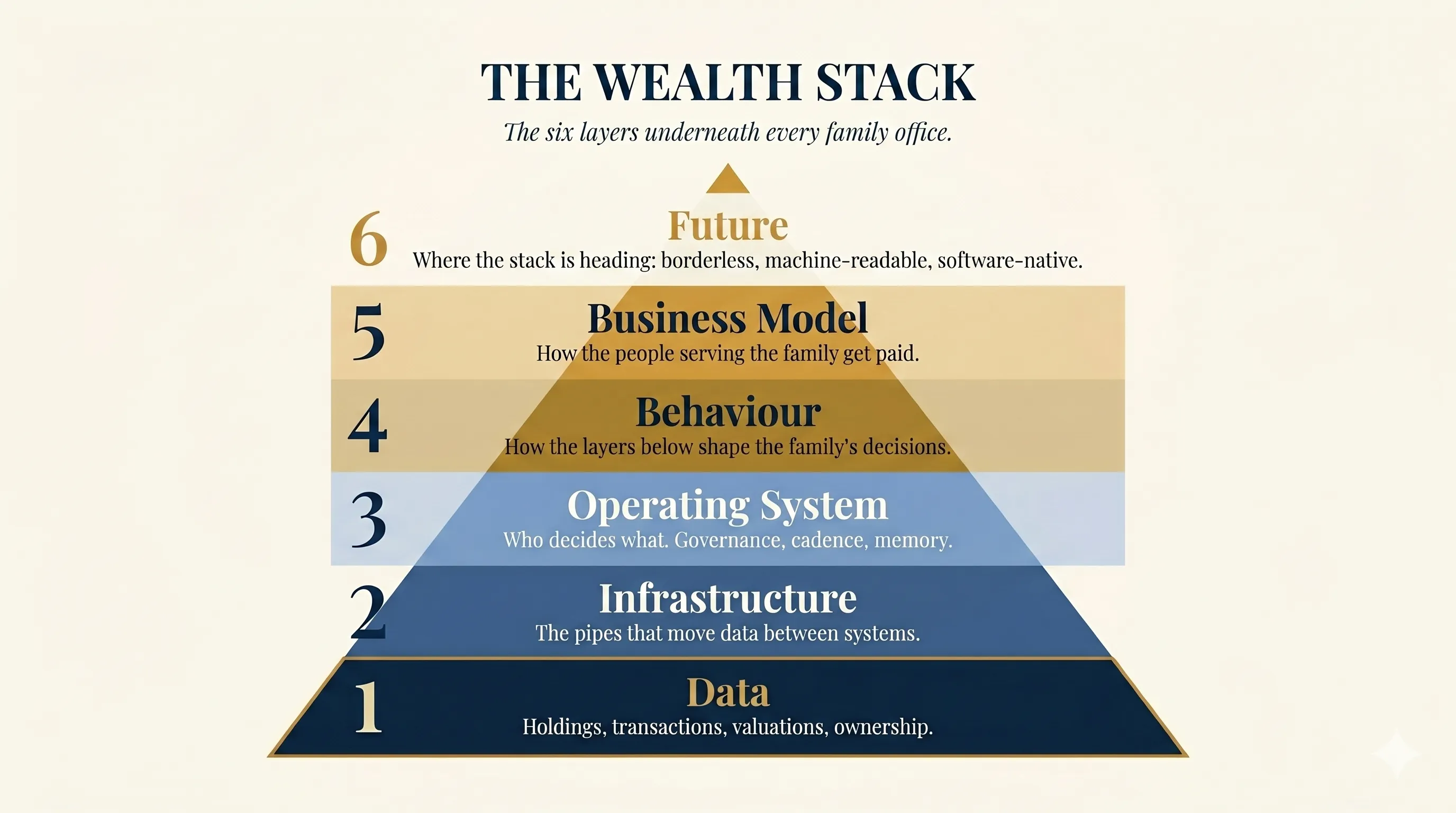

Six layers sit underneath the dashboard. Most families have all six in some form, even if nobody has named them. When wealth breaks — and it breaks in small ways constantly — it breaks at one of these layers. The work is locating which one.

1. Data

The bottom of the stack. Holdings, transactions, valuations, ownership.

Most of what a family office calls “data” is actually six or seven partial pictures that nobody has reconciled. CAS — your consolidated account statement — gives you mutual funds and equities held in your demat, and that’s the cleanest source you’ll get. PMS, your portfolio-management accounts, comes monthly or quarterly, in a PDF, with a unit-style holding statement that often disagrees with the underlying scrip-level breakdown if you ask for one. AIFs — your private funds — send drawdown notices over email and capital account statements once a quarter, sometimes late. Unlisted holdings sit at the last private round price, or whatever number the auditor used at year-end. Pledged shares need a separate pull. Foreign accounts — Singapore custodian, US brokerage from when the founder lived there — those don’t show up anywhere unless someone manually adds them.

Names don’t match across these sources. The trust is “Mehta Family Private Trust” in CAMS, “Mehta Family Pvt Trust” in KFin, and “MEHTA FAMILY TRUST” with three trailing spaces in the AIF’s records. PAN-matching solves some of this. The rest sits in a tab somewhere called “Name Mappings”. When somebody new joins the team, the mappings get re-learned, badly.

The honest answer to “what do we own” is almost always “give me three days.” When the answer turns up, you almost forget why you asked that question in the first place. That’s the data layer.

2. Infrastructure

The pipes that move data between systems.

For most Indian families, the infrastructure layer is one analyst, one Excel workbook, and a calendar reminder on the 5th of every month. The system is a person. When the analyst takes leave, the system goes on leave too.

The families that have bought software usually have a portfolio tracker that pulls CAS and equities and gives up on the rest. The PMS still goes in by hand. The AIF capital account is updated when somebody remembers to forward the email. Account Aggregator is real and useful for what AA covers — mostly banks, mutual funds, growing slices of insurance and pension. Unlisted, AIF and PMS aren’t on AA yet in any meaningful way. MFCentral works for funds. KFin and CAMS work if you’re patient with their portals.

The result is a partial pipe. The clean half of the wealth is automated. The messy half — usually larger in rupee terms for an HNI — is still manual. Reconciliation happens at month-end or quarter-end, and “reconciliation” usually means an analyst opening two files and squinting.

I have yet to meet a family office where the infrastructure layer was the thing they thought they were buying. They thought they were buying reporting. They got infrastructure that kind of works for the easy assets and quietly hands the hard ones back to a human.

3. Operating System

Who decides what. When the family meets. What gets escalated. Where the rules live.

This is the layer people forget exists, because it has no software. The operating system of a wealthy Indian family is usually the head of the family’s WhatsApp, the senior RM’s memory, and an annual meeting that happens nine months late.

The Investment Policy Statement — the one-page document that says “we will hold no less than X% liquid, we will not take single-position exposure above Y%, the investment committee approves anything above Z” — almost none of the families I know have one that is consistently followed. The ones that do have one drafted it during a private banker pitch in 2018 and haven’t opened it since.

Decision rights are unclear. Can the RM move ₹4cr between funds without asking? Probably. Can she move ₹20cr? She’ll call. Can she add a new AIF? The family head decides. Can she exit one? Murky. Most family offices run on “ask if you’re not sure” — which works, until the family head is travelling, or unwell, or no longer available.

Cadence is the other half of this layer. The portfolio tracker thinks daily. The advisor thinks quarterly. The family actually decides annually, usually triggered by the audit. None of these is wrong on its own; they just aren’t coordinated. So daily noise gets weight it shouldn’t have, and annual decisions get made on whatever happens to be on the screen the week of the audit.

When somebody asks “who runs your family office,” the honest answer for most families is “the senior RM at the wealth manager, and the family head’s gut.” That is a real operating system. It’s just not written down, and it has exactly one point of failure.

4. Behaviour

What the layers underneath do to the people on top.

A partner who watches a clean live dashboard at 7am every morning will trade more, not less. I’ve watched this happen. The partner isn’t undisciplined. The interface keeps presenting decisions that don’t need to be made, and after enough mornings, the question stops being “should I do anything?” and becomes “what should I do?”

The opposite failure is the family head who doesn’t look at all until the audit lands and then panics in October about decisions made in March. Both shapes come from the same root — what the lower layers do with attention.

Meera — the partner with the three equity numbers — went into the rest of her day a little uneasy. Not about the equity exposure itself, but because she didn’t know what else was hiding in the same gap, and she had a private, specific reason to be afraid of gaps. Anxiety scales with fragmentation. After a while, looking at the wealth becomes work.

The liquidity illusion is the other behaviour failure I see most often. “We have ₹40cr in cash” — yes, but ₹22cr is in an AIF Cat II with three more years of lock-up that nobody is modelling as illiquid, and ₹11cr is a real-estate down-payment that hasn’t been called yet but will be. The actual freely deployable cash is ₹7cr, and the family is committing to a ₹15cr private deal next month on the assumption that they have plenty of room. The arithmetic is fine. The family just isn’t seeing what they have.

5. Business Model

How the people serving the family get paid, and what that pays them to do.

I’ll keep this short because there’s a whole pillar on it later. The shape that matters here: the dominant business model in Indian wealth is still AUM-based, often dressed as advisory but compensated as distribution. The relationship manager who is the family’s main interface is paid by the AMC for some of what she sells, and by the bank for retaining the assets, and notionally by the family for advice.

Most RMs I know are honest. The argument here is structural. The business model decides what the RM has time to do. An RM serving 37 families cannot remember which child the family head trusts. She has to optimise for the conversations that hit her dashboard this week, which means the families with movement, not the families with continuity. The model rewards motion.

The business model layer is also where institutional memory leaks. When the senior RM moves firms — which she will, every three to five years — a decade of context walks out with her. The family discovers this six months later, when the new RM asks a question whose answer everyone used to know.

6. Future

Where the previous five layers are heading.

The thing most people get wrong about the future layer is treating it as a separate set of decisions. It isn’t. The future shape of a family’s wealth is determined right now by what the lower layers can carry. If your data layer can’t represent a Mauritius fund cleanly, you don’t own offshore — you own offshore on paper and a problem in practice. If your operating system runs on the head of the family’s memory, succession isn’t an estate-planning problem; it’s a system-extinction problem.

Two trends worth naming concretely.

First, the next generation of Indian wealth holders does not want to inherit a relationship with a wealth manager. They want to inherit a system they can log into. They are software-native, suspicious of intermediaries, and entirely willing to fire the family advisor if the credentials don’t transfer. Almost no current setup is built for this handover.

Second, the balance sheet is going borderless faster than most families realise. Children studying in the US who haven’t said whether they’re coming back. A GIFT City entity nobody quite understands. An equity grant in a Series C company headquartered in Singapore. An investment in a private AI company based out of Delaware. Five years from now this is the median wealthy Indian family, not the outlier. The data layer most families have today cannot represent it without breaking.

AI sits across all of this, mostly at the upper layers — it makes reports cheap, dashboards generatable, summaries instant. I wrote about that in more detail recently. What it doesn’t do is automatically fix the lower layers. A model can reconcile a CAS statement in seconds. It still doesn’t know that the steel-company block is the business Anand Mehta started in a rented shed in Hosur in 1987, or that he told his children — across a dinner table, never on paper — that those shares were not to be sold until Tara’s wedding was paid for.

Locating the floor

The reason the stack matters is diagnostic.

When something goes wrong — a number that doesn’t match, a decision that didn’t happen, an exit that came as a surprise — the temptation is to fix the visible layer. Get a better software. Make the dashboard more complex. Hire a better RM. Switch wealth managers. These fixes are cheap and feel like progress. They almost never solve the actual problem, because the actual problem was three layers down.

Meera didn’t need a new dashboard. When she finally walked the question down, the break wasn’t in the dashboard, and it wasn’t even the data — each of the three numbers was defensible. It was the operating system. Nobody had ever decided which number the family uses to make a decision.

She knew exactly what that gap could cost, because she had watched it cost them once. Fourteen months earlier, a capital call she hadn’t modelled came due on a real-estate fund the Mehtas had committed to — ₹9.2cr, payable in eleven days. On the screen, the cleanest way to raise it was obvious: trim the largest, most liquid line in the portfolio, a block of shares in the steel company. So that is what was done. It was a clean trade. It cleared in two sessions, and nobody flagged it, because nothing in any system knew that those were the shares Anand Mehta had told his children would not be sold until Tara’s wedding was paid for. He found out three weeks later, from his son, by accident. He didn’t shout. He just stopped forwarding the AIF emails.

That is what frightened her about Tuesday’s three numbers — not the ₹14cr spread, but the next steel block: a rule that lived in someone’s memory instead of in the system, waiting to be broken by a trade that looked entirely reasonable on a screen. The fix was never a better dashboard. It was one line — this holding is not sold without the family’s sign-off — and a single agreed number the family uses to decide. Building that is a six-month problem, not a six-week one. But once it exists, the screen can no longer be right and wrong at the same time.

If you want one thing to do this week — pick the last simple question that produced more than one answer in your family office. Walk it down the stack. Find the layer where it broke. It will almost never be the layer you expected.