Why Build Wealth Software In The Age Of AI

Anthropic CEO just said software is becoming worthless. We build wealth software, and we think he's right. Here's the Wealth Stack — a framework for which parts of wealth-tech AI eats, and which parts it makes far more valuable.

Recently, Anthropic CEO Dario Amodei said software is going to become “cheap, maybe essentially free.” He described a future where an application gets generated for a single meeting, used once, and thrown away. That sounds extreme, but the direction is obvious. AI is rapidly reducing the cost of:

- writing code

- generating interfaces

- building workflows

- summarizing information

- creating reports

- automating operational tasks

In my view, a large chunk of “wealth management” today is really a services business, coordinated by software. Relationship managers coordinate paperwork. Analysts reconcile statements. Operations teams chase PDFs and capital calls. Advisors spend hours stitching fragmented information into something a client can actually understand. AI is going to attack this layer aggressively, since most of this can be replaced by AI-driven intelligent software.

If your entire value proposition is dashboards, reporting, and workflow software, you should be worried. But after thinking about this for a while, I think the more interesting question is where AI struggles.

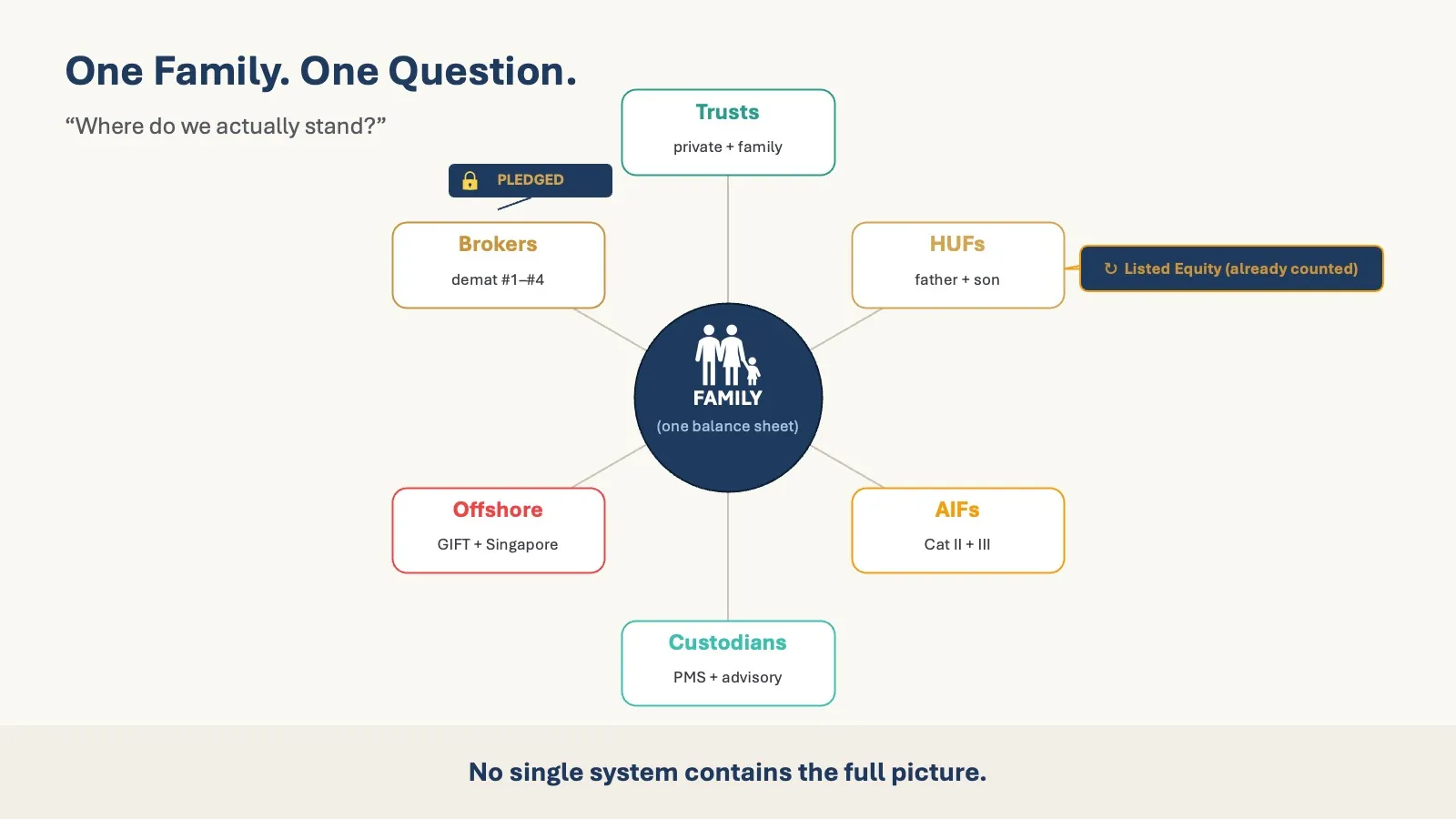

Wealth Was Never Just A Software Problem

Most discussions about wealth-tech software focus on the visible layer: dashboards, apps, reporting, portfolio views, notifications, etc.

But the operational reality underlying the beautiful dashboards is messy, very messy. Especially in India.

A single typically wealthy family may have:

- dozens of demat accounts across NSDL and CDSL

- several brokers

- PMS allocations

- AIF commitments

- trusts

- HUFs

- holding companies

- pledged shares

- offshore accounts

- private investments

- multiple wealth advisors & distributors, each seeing only one part of the picture

The dashboard is easy. Getting all the underlying reality to agree is the hard part.

The Coordination Layer Is Getting More Complex

This problem is getting more complex as Indian wealth becomes more sophisticated. Alternatives are growing rapidly. Family offices are becoming more common. Wealth structures are becoming more layered across generations, jurisdictions and entities.

At the same time, the operational layer is still held together in surprisingly manual ways:

- PDFs arriving late

- statements with inconsistent formats

- WhatsApp messages for capital calls

- stale private asset valuations

- spreadsheets passed between teams

- verbal instructions that never make it into systems

One Category II AIF sends a capital call over WhatsApp. The investor name on the PDF does not exactly match the KRA database. The AI can parse the PDF. But who decides whether the mismatch matters? Who knows whether that allocation belongs to the trust, the HUF, or the Karta personally? Who remembers that the family had already reserved liquidity elsewhere because another fund drawdown is expected next month?

This is where the situation becomes interesting.

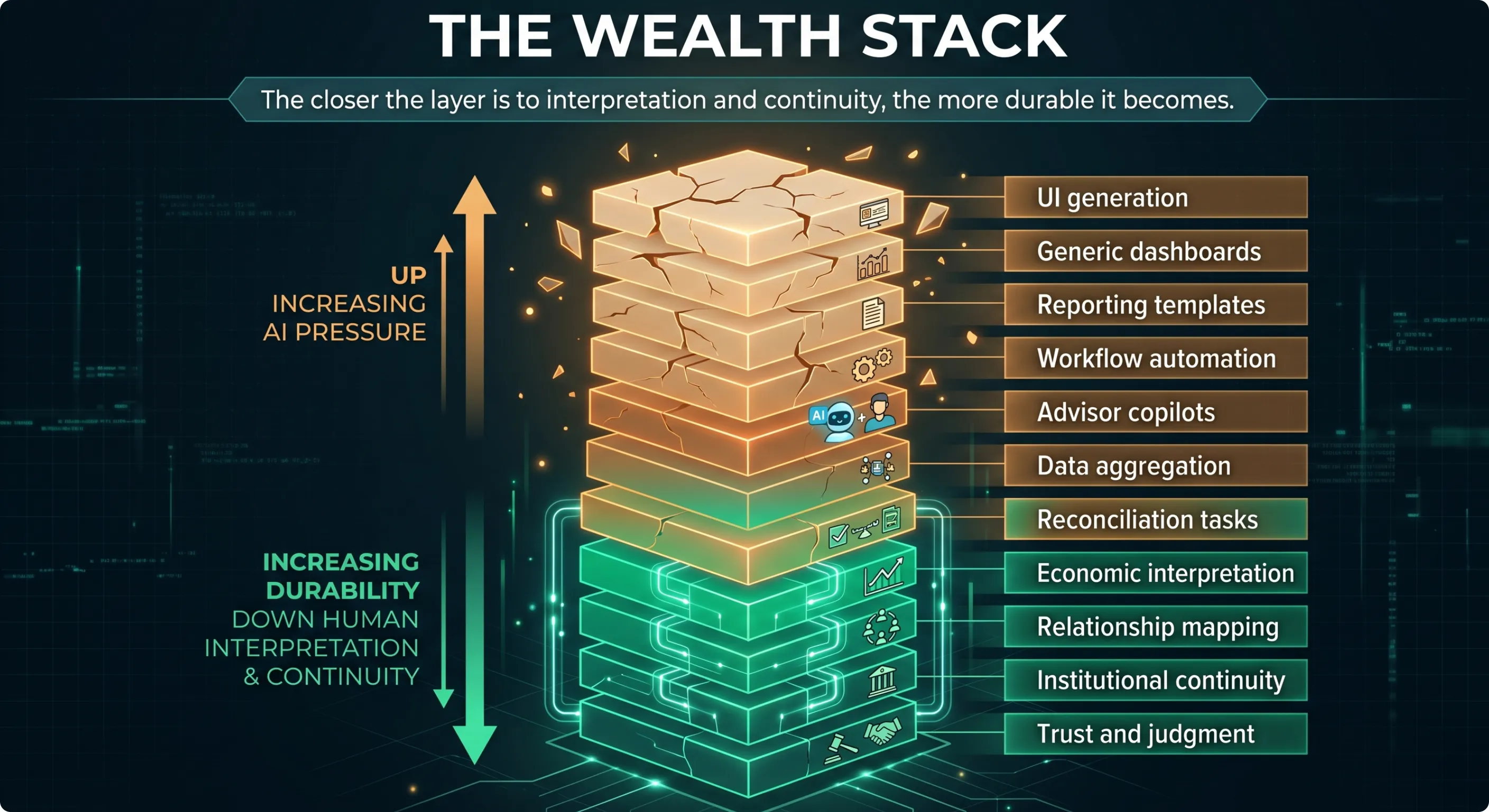

The Wealth Stack

AI does not affect every layer of wealth technology equally. Some layers are becoming commodities very quickly.

| Layer | AI Pressure |

|---|---|

| UI generation | Very High |

| Generic dashboards | Very High |

| Reporting templates | High |

| Workflow automation | High |

| Advisor copilots | High |

| Data aggregation | High |

| Reconciliation tasks | Moderate |

| Economic interpretation | Lower |

| Relationship mapping | Low |

| Institutional continuity | Low |

| Trust and judgment | Very Low |

The upper layers of the stack are increasingly easy to generate. The lower layers still depend heavily on context, interpretation and accumulated understanding.

The Counterargument Matters

There is an obvious pushback to all this. One is that maybe the fragmentation itself disappears.

India is already moving toward cleaner financial infrastructure through:

- Account Aggregator frameworks

- standardized RTA feeds

- MFCentral

- API-based data access

If financial data becomes standardized and portable, then aggregation and reconciliation become cheaper too. I think that is directionally true. A lot of what wealth-management software does today will eventually become infrastructure plumbing.

This is not a defensible moat. History gives plenty of examples.

Telecom operators owned massive infrastructure. Messaging and voice eventually moved to software layers like WhatsApp and Skype. Banks owned the ledger and the money. Payments increasingly shifted to layers like UPI and Stripe.

The same thing can happen in wealth. Owning operational complexity is not automatically a moat.

Where The Complexity Actually Survives

However, even if public-market data becomes standardized, private wealth remains deeply idiosyncratic. The hard part is no longer pulling the data, but understanding what the data actually means.

One family keeps assets in an HUF because of tax advice from fifteen years ago. Another moved some holdings outside the trust structure after a family dispute. A founder refuses to sell a concentrated stock position because it represents control of the business, not portfolio exposure. This is where we need to draw the distinction between intelligence and judgment.

In our view, AI increasingly provides intelligence:

- summarization

- reconciliation

- analysis

- workflow coordination

- anomaly detection

But AI cannot be a substitute for judgment. Judgment involves:

- undocumented context

- incentives

- emotional realities

- family dynamics

- ambiguity

- tradeoffs between technically correct and practically workable

You can dump ten years of emails into an LLM. That still does not tell it which sibling the family head actually trusts with money. It cannot tell you the family created it after a painful inheritance dispute and nobody wants to reopen the issue. That layer of context usually exists partially outside the system. And it matters more than people think.

Continuity Matters More Than Interface Quality

At the risk of repetition, let me state that a lot of wealth platforms still compete on cleaner dashboards, prettier reports and smoother interfaces. Those things are becoming cheaper very quickly. The more durable value may sit elsewhere.

Can the system preserve continuity when the relationship manager leaves? Can it trace economic ownership across trusts, HUFs and holding companies without forcing the family to rebuild everything from scratch? Can it retain historical reasoning behind decisions? Can it show not just what the family owns, but why structures were created in the first place?

That is harder to automate than people assume, especially because much of the important context in wealth management is never fully written down. Even what is written down is captured as “notes” or “remarks” - not easy to be able to use it for reasoning with AI.

What AI Probably Changes

So, yes, AI will reduce the cost of large parts of wealth management. Margins around these layers will compress. But the systems that survive will probably combine:

- interoperable infrastructure

- durable historical records

- relationship mapping

- operational context memory - this is like a super-human with infinite memory and infinite context

- AI-native orchestration

- human judgment sitting on top of machine intelligence

The future probably contains infinitely generated inexpensive interface, along with nearly free high quality advice on what needs to be done. The difficult part will still be interpreting economic reality across fragmented systems, incomplete information and human relationships. That was always the harder problem. AI just makes the distinction more visible.